- Afghanistan

- Africa

- Budget Management

- Defense

- Economy

- Education

- Energy

- Environment

- Global Diplomacy

- Health Care

- Homeland Security

- Immigration

- International Trade

- Iraq

- Judicial Nominations

- Middle East

- National Security

- Veterans

|

Home >

News & Policies >

February 2002

|

February 15, 2002

Council of Economic Advisers' Report

With the enactment in 2001 of the Economic Growth and Tax Relief Reconciliation Act ("Tax Relief Act"), the President has laid a strong foundation for long run growth. This tax relief has provided powerful stimulus for the future, with reductions in marginal tax rates that improve incentives and leave in the hands of Americans a greater share of their own money to spend on consumption, education, retirement investment, or whatever else they may prefer.

The tax relief also has provided valuable stimulus to economic activity in the short run. The quick enactment last year of the President's tax relief plan softened the recessionary headwinds in 2001 and has helped to put the economy on the road to recovery in 2002. Various provisions of the Tax Relief Act have helped to boost aggregate demand.

The first reduction in marginal tax rates was reflected in lower withholding during the second half of the year. In addition, the lower tax liability of the new 10 percent tax rate bracket, which was carved out of the 15 percent rate bracket, came in the form of rebate checks totaling $36 billion, which were mailed during the second half of 2001. The timing of rebates and the reductions in withholding proved propitious: they added significant economic stimulus by boosting consumers' purchasing power during a period of sluggish economic activity.

The short-run economic growth effects of the Tax Relief Act have been significant without this tax relief, the 2001 recession would have been deeper and longer. Quantitatively, the rebate checks and the reduced taxpayer liabilities (including the reduction in the marriage penalty for earned income credit recipients and the initial increase in the child credit) totaled $57 billion in 2001 and $69 billion in 2002.

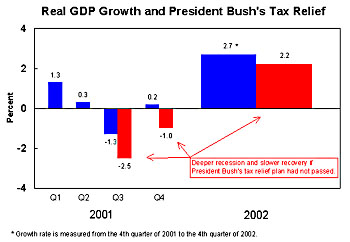

The following chart illustrates the size of the growth

benefits. The economic slowdown that began in mid-2000

continued in 2001. Without the Tax Relief Act,

third-quarter growth would have been much worse, contracting at a 2.5

percent annual rate instead of the reported 1.3 percent

rate. And,in the fourth quarter, real GDP would have fallen 1 percent instead

of the advance estimate of 0.2 percent growth.

In sum, the President and Congress delivered important tax relief in 2001, giving a welcome boost to jobs and income. As a consequence, the recession?which the National Bureau of Economic Research dated as having started in March of 2001?has been more mild and will likely turn out to be shorter than it otherwise would have been without the tax relief.

Looking forward, the 2001 tax rate reductions were just the first step in a series of income tax rate reductions to be phased in by 2006; by that year the 39.6 percent tax rate will have dropped to 35 percent, the 36 percent rate to 33 percent, the 31 percent rate to 28 percent, and the 28 percent rate to 25 percent. The future rate cuts increase expected disposable income.

The tax cut package also increased the incentives for saving, bequests to heirs, and investment. Higher IRA and 401(k) retirement contribution limits are to be phased in. Beginning in 2002 and continuing through 2009, the highest estate tax rates will be reduced and the effective exemption amount increased, reducing an important impediment to the growth of entrepreneurial enterprises and the overall accumulation of wealth.

In 2010 the estate tax will be eliminated. Small businesses have benefited from the lowering of individual income tax rates for owners of flow-through business entities such as sole proprietorships and partnerships. In 1998 there were close to 24 million flow-through businesses in the United States, including 17.1 million sole proprietors, 2.1 million farm proprietorships, 1.9 million partnerships, and 2.6 million S corporations. By 2006, when the tax cut will be fully phased in, the Treasury Department estimates that over 20 million tax filers with income from flow-through entities will receive a tax reduction.

Finally, the President's tax cut strengthened families and has reduced the burden of financing education. The marriage penalty was reduced for earned income credit recipients, and the child tax credit increased from $500 to $600 per child in 2001 and will gradually increase to $1,000 by 2010. Adoption credits have been doubled in 2002 from $5,000 per child in 2001; in addition, this credit will apply to more taxpayers because the income threshold at which the credit begins to be phased out is $150,000, up from $75,000. Contribution limits for education savings accounts (formerly called educational IRAs) were raised to $2,000, and distributions were made non-taxable. The law also increased the income phase-out range for student loan interest deductions and made certain higher education costs tax-deductible for households with less than $130,000 in income.

As a consequence, the Tax Relief Act has raised the prospects of a solid recovery in 2002 by boosting economic growth by 0.5 percentage point, lifting the expected growth rate from 2.2 percent to 2.7 percent. Moreover, by the end of 2002, the President's tax relief will have helped the private sector to create 800,000 more jobs than there otherwise would have been.

Some policymakers have advocated canceling the scheduled tax cuts. Raising taxes during a period of slow economic growth, however, does not make economic sense. Raising taxes would not only lower long-run growth prospects but also jeopardize a recovery. The nascent recovery is still vulnerable and can be derailed by adverse shocks such as those arising from a tax increase.

A tax increase would be detrimental for several important reasons. First, an increase in taxes would sap the economy of demand, as individuals and small businesses would see a decline in their after-tax income. As an illustration, the Council of Economic Advisers estimates the impact to be 0.7 percent of GDP in 2003 and about 500,000 jobs. Second, cancellation would break a promise made less than a year ago and could adversely affect consumer and business confidence about the future.

The rebound in economic activity since the terrorist attacks last September has been a testament to the resiliency of our Nation's market-based economic system. Good policies that support this system should not be taken for granted. Pro-growth policies, such as the President's plan for permanent tax relief, are important because they give short-run and long-run incentives to the private sector to create jobs, raise income, and restore prosperity.